Federal (T1 Return) – Scholarship Exemption

- Full-time students: Scholarships, fellowships, or bursaries are non-taxable if enrolled in a qualifying educational program during the tax year, or in the year immediately before or after.

- Part-time students: Exemption limited to tuition and program-related material costs.

- Non-qualifying students: $500 exemption; amounts over $500 are taxable.

- Elementary/secondary school: Scholarships and bursaries are not taxable.

Quebec (TP-1 Return) – Scholarship Exemption

- Line 154: Report the total amount from Box O (code RB) of the RL-1 slip as Other Income, regardless of student status.

- Line 295: Deduct the portion of the scholarship that is exempt. For most full-time students, this will equal the amount reported on Line 154.

Example :

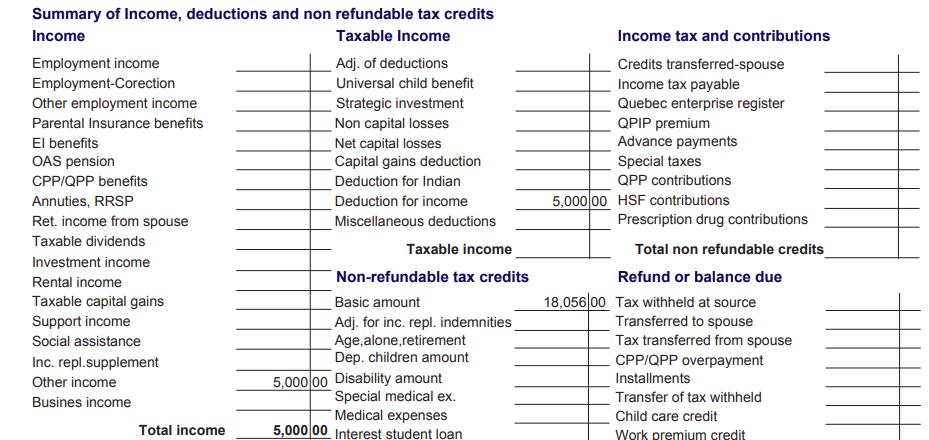

Aimé is full-time university student receives a $5,000 scholarship; federally, it appears in Box 105 of the T4A slip and is fully exempt (not reported on Line 13010), while provincially, it is reported on Line 154 of the TP-1 and claimed as a $5,000 deduction on Line 295, making it non-taxable.

How to do on TaxTron?

In the Income section, enter the amount from the T4A slip. Then, select 'Yes' to confirm an RL-2 slip was received, and choose 'full-time scholarship'.

Posted on 6 January 2026