Some employers require employees to cover certain expenses necessary to perform their job duties. Whether salaried or commissioned, the employer must complete and sign Form T2200, Declaration of Conditions of Employment, to confirm which expenses are required and whether reimbursement has been provided.

Salaried employees can deduct specific employment-related expenses on line 22900 of the income tax return to reduce taxable income. A loss cannot be claimed on line 22900, but any unused amounts may be carried forward to future years.

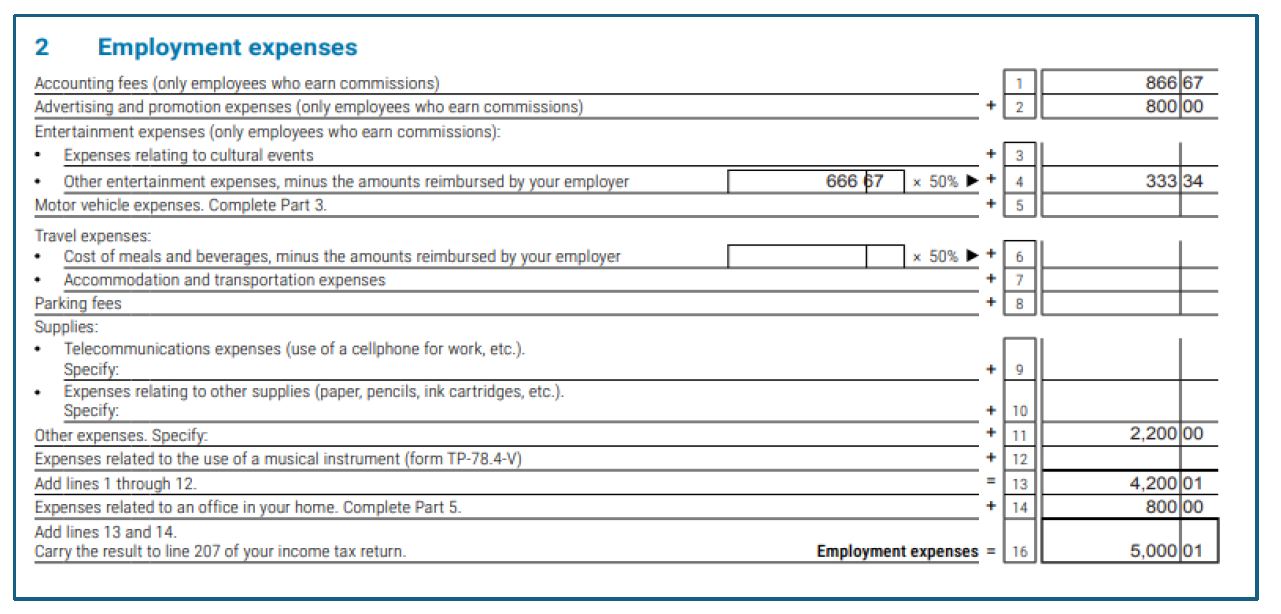

Accounting and Legal Fees (only for Commission employees):

Reasonable accounting fees paid for preparing an income tax return and legal fees incurred to collect or establish a right to collect salary or wages are deductible. Legal fees paid to establish the right to collect salary or wages are deductible, but the claim must be reduced by any amount reimbursed or awarded by a court.

Travel Expenses:

Fifty percent of meal and beverage costs and 100% of lodging expenses incurred while away from home are deductible. Travel costs are deductible if all of the following conditions are met:- Work was required away from the employer’s regular place of business.

- Travel to multiple locations was necessary to perform duties.

- Travel expenses were paid personally.

- A signed Form T2200 or TP64 is held.

Transportation costs such as airfare, train, or bus tickets are also deductible, while motor vehicle expenses are claimed separately. Up to three meals per day can be deducted using either:

- The detailed method (actual meal costs supported by receipts), or

- The simplified method ($17 per meal, up to $51 per day).

Parking:

Parking expenses at your primary work location are not deductible. However, you may deduct parking costs incurred when you are required to work away from your main location—for example, when meeting a client.

Supplies:

Consumable supplies that are used directly in work are deductible including:- The employment-related portion of your cellphone service plan.

- Office supplies (e.g., pens, paper).

- Special work-related clothing that is not suitable for personal use (e.g., clown costumes, wigs, nurse scrubs).

- Capital expenses (e.g., computers, printers, headsets) are also not deductible under employment expenses.

Salary Expenses:

If the employment contract requires hiring an assistant, wages paid are deductible, provided this is specified in Form T2200 or TP64. Income tax, EI, and CPP (or QPP) must be withheld and remitted, and a T4 slip must be issued to the CRA (and an RL-1 for Québec).

Office Rent:

If the employment contract requires renting a separate office space, the rent attributable to work is deductible. This differs from home office expenses: for example, if 10% of a home is used for work, 10% of the rent may be deducted. However, rent for a separate office used exclusively for the job is fully deductible.Home Office Expenses:

Home office expenses may be claimed when required by the employment contract and personally paid. To qualify, the workspace must meet one of the following tests:

Mainly used for work: The home office is used for work more than 50% of the time for at least four consecutive weeks during the year.

Exclusively for work: The space is used solely to earn employment income and is regularly and continuously used for meetings with clients, customers, or other individuals.

- Utilities (heat, electricity, water)

- Rent

- Maintenance (current expenses only)

- property taxes (only for Commission employees),

- home insurance (only for Commission employees) or

- mortgage interest (only for self employment)

Motor Vehicle Expenses:

Motor vehicle expenses are deductible when work requires travel away from the employer’s regular place of business, the expenses are personally paid under the employment contract, and no non-taxable benefit has been received for the same costs. Commuting between home and the regular workplace is not considered work-related travel. Eligible expenses include:

- Fuel (gas, oil, propane)

- Maintenance and repairs

- Insurance

- License and registration fees

- Capital cost allowance (depreciation)

- Interest on a loan used to purchase the vehicle

- Eligible lease costs

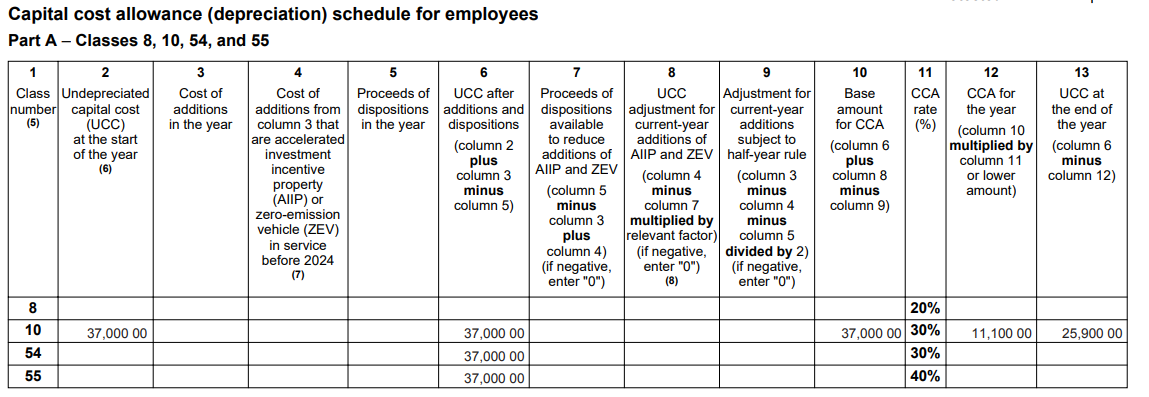

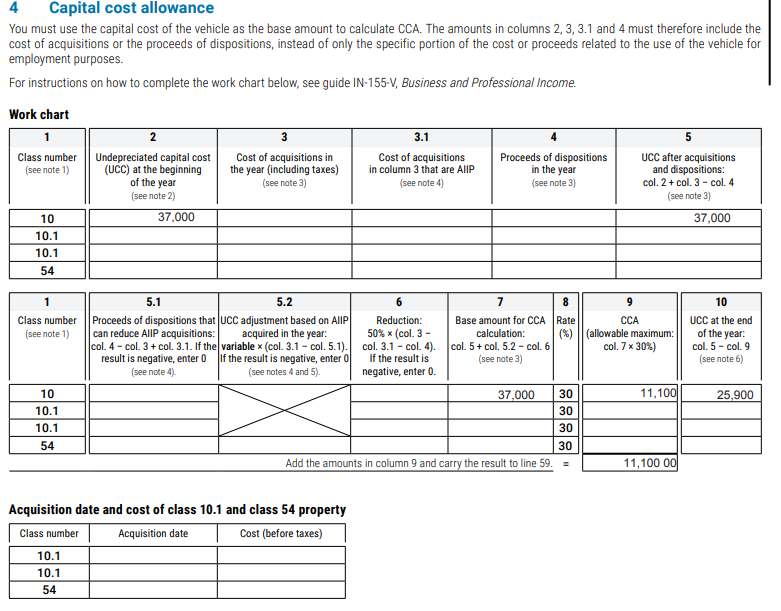

Capital cost allowance:

Capital Cost Allowance (CCA) is a tax deduction that allows businesses and some employees to write off the cost of eligible depreciable property, such as motor vehicles and other equipment, over a number of years. The specific rules, classes, and rates for CCA differ for federal and Quebec tax returns.

CCA classes and rates:

The CRA groups depreciable properties into different classes, each with its own CCA rate. A similar classification system exists for Quebec tax purposes.

Motor vehicles

- Class 10 (30%): Motor vehicles and some passenger vehicles that do not meet the criteria for Class 10.1.

- Class 10.1 (30%): Passenger vehicles that cost more than a specific capital cost limit (before sales tax). For 2024, the limit is $37,000. Each vehicle in this class is treated separately.

Zero-emission vehicles (ZEVs):

Special classes with enhanced first-year CCA rates apply to eligible ZEVs.

- Class 54 (30%): For ZEVs that would otherwise be in Class 10 or 10.1. A capital cost limit applies ($61,000 for 2024).

- Class 55 (40%): For ZEVs that would otherwise be in Class 16.

- Enhanced CCA rates on ZEVs acquired before 2028 are being phased out.

Other equipment:

Class 8 (20%): General-purpose equipment, machinery, furniture, and appliances.

Calculating and claiming CCA: Federal & Quebec

- Half-year rule: For many asset classes, you can only claim 50% of the CCA you would otherwise be entitled to in the year you acquire the asset. This does not apply to zero-emission vehicles and other specific classes.

- Calculate CCA: Complete Form T777, including the CCA charts (Area A, B, or C). Your claim is based on the undepreciated capital cost (UCC) of each asset class.

- Report deduction: Enter the total CCA amount on line 22900 of your T1 return

Example :

David, a commission-based sales representative in Montreal, Quebec, required to use his personal vehicle and laptop for work, has Tech Solutions Inc. sign Form T2200 and TP64.3-V; in 2025, opening UCC for class 10 is $ 37,000 and a laptop for $2,000 (Class 50), drives 40,000 km total with 30,000 km for business (75% business use)Answer: Federal CCA on the motor vehicle as $37,000 × 30% × 75% = $11,100 on Form T777 and same amount on Form TP-59-V. As an employee, David cannot claim CCA on computer. However, if he is leasing/rental the computer, then the leasing expenses are deductible.

How to do in TaxTron?

Enter the amount from the T4 slip in the Income section. Select “Yes” to indicate that an RL-1 slip was received, and under Deduction Tab, choose Work Expenses and choose appropriate category.

Commission Employee

Commission employees can deduct a wide range of employment-related expenses by completing Form T777, Statement of Employment Expenses, and claiming the total on line 22900 of the T1 tax return and line 207 of TP1 tax return. Compared to salaried employees, the list of deductible expenses for commission employees is broader.

Expenses related to commission Income

- Accounting and legal fee: Reasonable accounting fees paid for preparing an income tax return and legal fees incurred to collect or establish a right to collect salary or wages are deductible.

- Advertising and promotion: Includes gifts and promotional items provided to clients.

- Bonding premiums: Bonding and liability insurance premiums is tax deductible.

- Entertainment: 50% of client entertainment costs are deductible.

- Equipment leasing: Lease cost related to equipment, computers, cell phones, fax machines, or other equipment.

- Medical underwriting fees: Payments for items such as X-rays and heart diagrams related to underwriting your customers' risks.

- Home office expenses: Commission employees may deduct a portion of home insurance and property taxes.

- Training expenses: The course must maintain, upgrade or update your existing skills or qualifications

Deduction Limit – The “Salesperson’s Dilemma”

For most expenses, the deduction cannot exceed the commission income earned during the year. However, interest and CCA on a motor vehicle are not subject to this limit. If expenses subject to this limit exceed commission income, it may be more beneficial to claim expenses as a salaried employee, which restricts certain sales-related deductions but removes the commission income cap for other eligible expenses.

GST/HST/QST Rebate

You may be eligible for a rebate of the GST/HST/QST paid on eligible employment expenses by filing Forms GST370, VD358 Employee and Partner GST/HST Rebate Application.

Quebec (Revenu Québec):

Commission employees in Quebec follow similar rules but must use provincial forms to claim expenses.

- Forms: Complete Form TP-59-V, Employment Expenses of Salaried Employees and Employees Who Earn Commissions and attach the employer-certified Form TP-64.3-V, General Employment Conditions.

- Deduction limit:/ As at the federal level, certain expenses are limited to the amount of commissions reported on the RL-1 slip.

- Exempt expenses: Some deductions are not subject to this limit, including CCA and interest on a vehicle, certain home office expenses, supplies, and motor vehicle expenses.

- QST rebate: A rebate for Quebec Sales Tax (QST) paid on eligible expenses can be claimed using Form VD358-V, Québec Sales Tax Rebate for Employees and Partners.

Example :

Marie-Claire Dubois, a Québec commission employee earning $50,000 (Box 42 T4 / Box M RL-1), incurs $800 accounting fees, $500.01 legal fees, $1,200 advertising, $300 bonding premiums, $1,000 client entertainment (50% deductible = $500), $2,400 equipment lease, $1,200 home office, and $600 training.

Answer: Marie can claim expenses of $7,500.01 on each federal and Québec returns.

Example :

All other information is same as above but Marie ‘s Box 42 shows $5,000.01 as commission income.

Answer: Total deductible expenses are capped at $5,000.01 for both federal and Québec return due to the commission income limit.

Posted on 8 January, 2026